In recent years, the global medical device industry has shown three major characteristics in mergers and acquisitions: 1) Increasingly larger mergers, leading to higher concentration and fewer potential acquisition targets; 2) The scale of product and market crossover is increasing, with significant structural adjustments in the main market; 3) The acceleration of cross-border mergers and acquisitions, with a significant increase in Chinese acquisition targets.

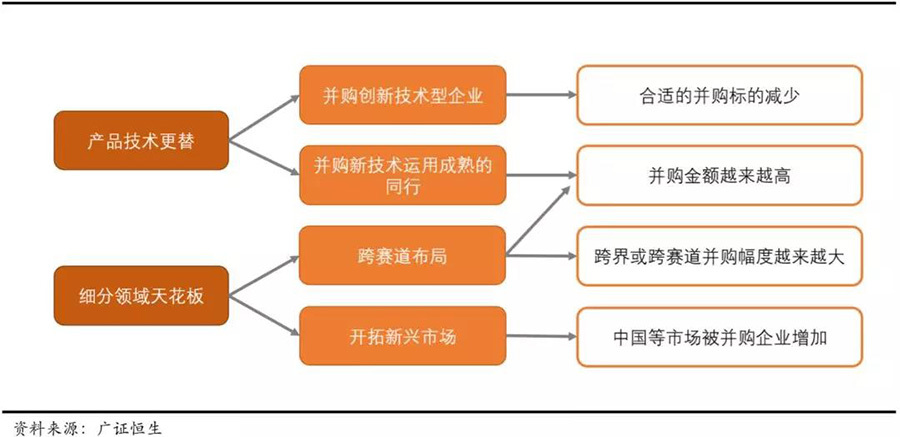

We believe this is mainly due to two major driving forces:Product technology updates and iterations + the ceiling effect in segmented fields..

First, there is the update and iteration of product technology within the industry. Unlike the product cycle of over 10 years for pharmaceuticals, the technology in the medical device field is relatively fast, with shorter product cycles. Each new product launch often has a disruptive impact on the previous generation of products. Therefore, the degree to which medical device companies master cutting-edge technologies in this field will greatly affect their future market share and position. In addressing this issue, the main strategies of medical device giants are: 1) Continuously acquiring innovative technology companies to strengthen external R&D; 2) Merging with competitors that already possess mature technologies. This includes both proactive prevention and remedial measures. The acquired companies are either already industry leaders or still in the technology development stage.

Secondly, the ceiling effect in segmented fields is another major driving force for mergers and acquisitions among medical device giants. Although the medical device industry has reached a massive scale of $400 billion, it has many segmented fields and complex product types, including simpler products like hemostatic sponges and disposable syringes, as well as complex large devices like medical magnetic resonance imaging (MRI) equipment. Currently, the first-level classification of medical devices includes over 20 segmented fields such as IVD and cardiovascular, with products used for different diseases, and the demands of different patients vary greatly. This leads to medical device companies often facing the pressure of industry segmentation ceilings and challenges from cross-border competition.

In this regard, medical device giants also have two major countermeasures:1) Expanding into emerging markets to raise the industry ceiling; 2) Enriching their product matrix through cross-market and cross-border mergers and acquisitions. Therefore, in recent years, cross-border and cross-industry mergers and acquisitions have been continuously increasing..

▽ Main issues faced by medical device giants and countermeasures.

Increasingly larger mergers lead to higher concentration and fewer potential acquisition targets.

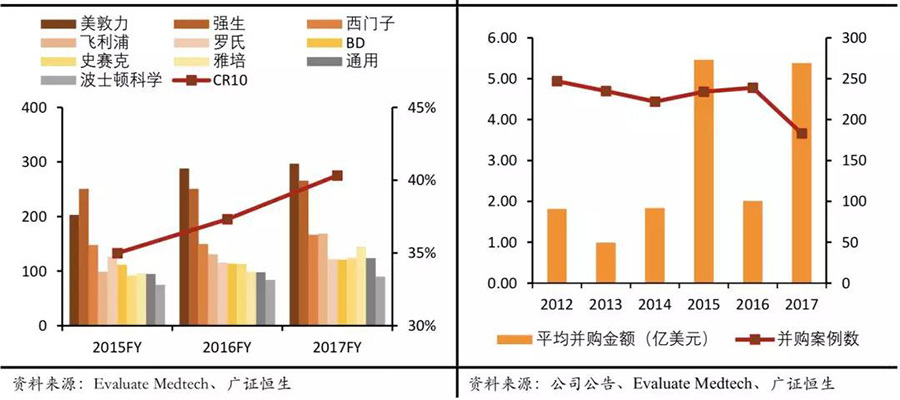

Global mergers and acquisitions in the medical device industry are showing increasingly larger trends, with higher industry concentration.In 2014, medical device giant Medtronic acquired Covidien for a record price of $42.9 billion, surpassing Johnson & Johnson in revenue scale to become the world's number one in the medical device industry.In the following years, mergers and acquisitions continued to ferment in the medical device industry. Industry giants achieved strong alliances through mergers and further enhanced their status in the industry. According to statistics, the global medical market CR10 rose from 35% in 2015 to 40% in 2017.

The number of substantial acquisition targets is continuously decreasing. In the past three years, the total amount of global medical device mergers and acquisitions has significantly increased, with 2015 being the peak, where the total amount exceeded $100 billion, and the average acquisition amount approached $550 million. At the same time, the number of mergers and acquisitions is on a downward trend. In 2017, the total amount of mergers and acquisitions in the global medical device industry was $98.5 billion, about twice that of 2016, but the number of mergers and acquisitions actually decreased by 20% compared to 2016. As the trend of mergers and acquisitions in the global medical device industry intensifies, the scale of leading enterprises continues to grow, resulting in a continuous decrease in the number of substantial acquisition targets, thus driving the amount of individual acquisition cases in the industry to rise.

▽ Revenue scale of industry giants continues to increase (in hundreds of millions) & the number of mergers and acquisitions decreases while the average acquisition price continues to rise.

The scale of product crossover and market crossover is increasing, with structural adjustments in the main market.

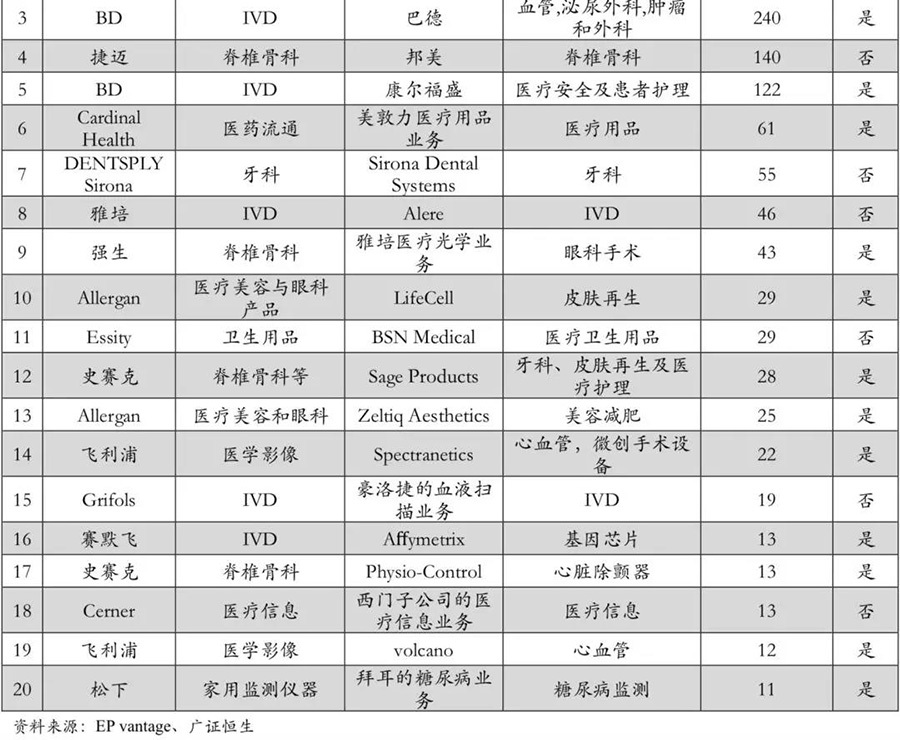

The scale of product crossover and market crossover is increasing. In recent years, cross-industry mergers and acquisitions have become the main direction for medical device giants. Whether in terms of products or markets, industry giants are achieving increasingly larger cross-industry expansions and competition through mergers and acquisitions. In the top 20 mergers and acquisitions in the past three years, 70% are strong alliances from different segmented fields of medical device giants. Among them, Medtronic and Covidien have teamed up to build a commercial empire that almost covers the entire field of medical devices; IVD leaders like Abbott and BD have also strengthened their layouts in cardiovascular and oncology through mergers and acquisitions. It can be seen that in recent years, the mergers and acquisitions of medical device giants have shown characteristics of increasing scale in product crossover and market crossover.

▽ Increasing number of cross-border mergers and acquisitions in the global medical device market.

Giants are making significant asset purchases while also divesting large-scale business units. In recent years, medical device giants Medtronic, Abbott, and Siemens have respectively divested their medical supplies, optical medical, and medical information businesses. Particularly in 2017, among the top 10 mergers and acquisitions, 4 were related to the divestiture of business units by industry giants. In the past three years, while medical device giants have been acquiring assets to expand their scale, they have also been divesting businesses to improve corporate efficiency, showing an overall trend of "gaining muscle while losing fat."

▽ Major giants begin to divest businesses.

There have been noticeable structural adjustments between markets. In terms of merger direction, compared to the merger trends in the industry before 2015, there has been a certain degree of structural change in the merger markets.Among them, IVD, surgical equipment, and medical aesthetics have been the hot spots for mergers and acquisitions in the past three years.In mergers and acquisitions with amounts greater than $1 billion, the above three markets accounted for 17.1%, 15.4%, and 4.4% of the total merger and acquisition amount, respectively, showing a significant increase compared to the proportion of merger and acquisition amounts before 2015. On the other hand, the merger speed in markets like cardiovascular and spinal orthopedics has shown a certain degree of slowdown, with the cardiovascular field being the most obvious, dropping from a proportion of 16.5% before 2015 to 3.6% in the past three years. In recent years, although the main mergers and acquisitions in the medical device industry are still focused on the main markets, there have been noticeable structural adjustments between markets.

▽ Large-scale mergers and acquisitions are still focused on the main markets, but there are clear structural adjustments between markets.

The acceleration of cross-border mergers and acquisitions, with a significant increase in Chinese acquisition targets.

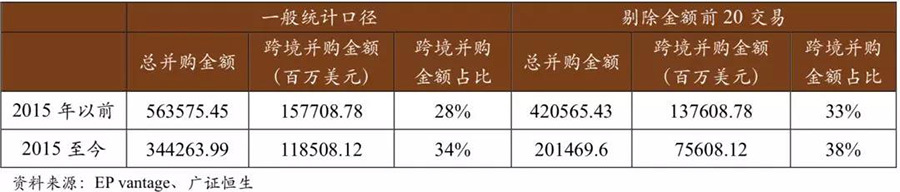

Cross-border mergers and acquisitions have shown a noticeable acceleration. In recent years, in the mergers and acquisitions of the medical device industry, both in terms of acquisition amounts and proportions, there has been a significant increase compared to the industry mergers and acquisitions before 2015. According to our statistics, in the industry mergers and acquisitions before 2015, the amount of cross-border mergers and acquisitions accounted for 28% of the total merger and acquisition amount, while in the merger transactions from 2015 to now, this proportion is 34%. Excluding individual transactions with excessively large amounts, this proportion is 33% and 38%, which is 5-6 percentage points higher than before 2015. Overall, in recent years, the industry mergers and acquisitions have shown characteristics of accelerating cross-border merger transactions.

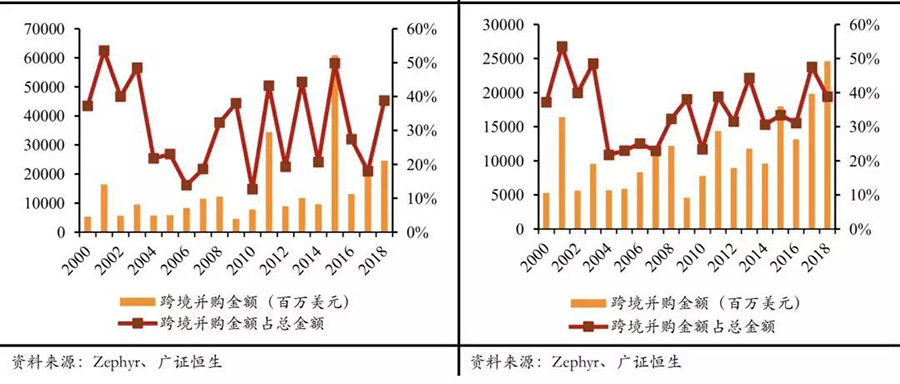

In recent years, the industry has shown a trend of accelerated cross-border mergers and acquisitions.

The acceleration of cross-border mergers and acquisitions is evident; even after excluding the top 20 transactions by amount, the acceleration remains significant.

The targets of mergers and acquisitions are concentrated in Europe and the United States, with a significant increase in the number of Chinese companies being acquired. In terms of the geographical distribution of acquisition targets, they are still concentrated in the U.S. and Europe. In the past three years, the acquisition amount of U.S. domestic targets accounted for as much as 62.2% of the total amount (if excluding the Medtronic acquisition of Covidien, this proportion is 71.1%), while the acquisition amount of European targets is generally around 20%. This continues the long-standing pattern where acquisition targets in the medical device sector mainly come from the U.S. and Europe. However, in recent years, the number of acquisition targets in China has significantly increased. Since 2015, China has produced 376 acquisition targets with an acquisition amount exceeding $1.3 billion, while in the nearly twenty years before 2015, China produced less than $300 million in acquisition targets. It can be seen that in the past three years, domestic companies' capital attention has greatly increased.

Acquisition targets mainly come from the U.S. and Europe, and the capital attention of Chinese companies has increased in recent years.

Motives for Mergers and Acquisitions

Motive for Mergers and Acquisitions One: Replacement of Product Technology.

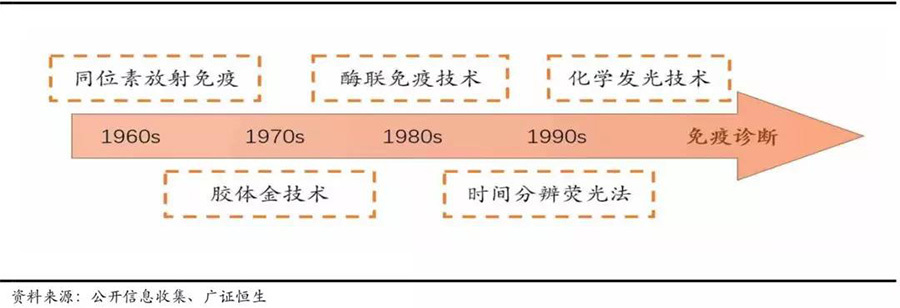

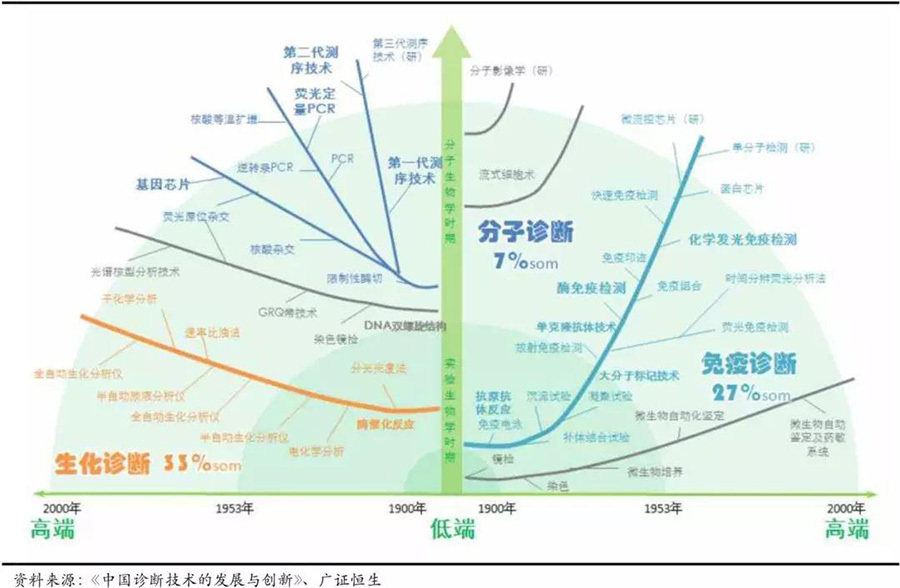

The technology and products in the medical device field are always undergoing rapid updates and replacements. Compared to pharmaceuticals, which have a long research and development cycle of generally 10-15 years and slow product updates, medical device technology matures quickly, and the product iteration cycle is short. Large enterprises are slow to turn around, while small and medium-sized enterprises have unique advantages in external research and development. Taking the IVD field as an example, the development of the industry is accompanied by advancements in biochemistry, immunology, molecular biology, etc., and can be divided into three development stages. The first stage is the budding period before the 20th century, using some traditional medical diagnostic technologies; the second stage is the early 20th century, when in vitro diagnostics gradually emerged with the development of modern medicine and the discovery of enzyme-catalyzed reactions and antigen-antibody reactions. The third stage, after 1953, saw the application of technologies such as the DNA double helix structure, monoclonal antibody technology, and macromolecular labeling technology, which propelled the entire in vitro diagnostic industry to leap forward.

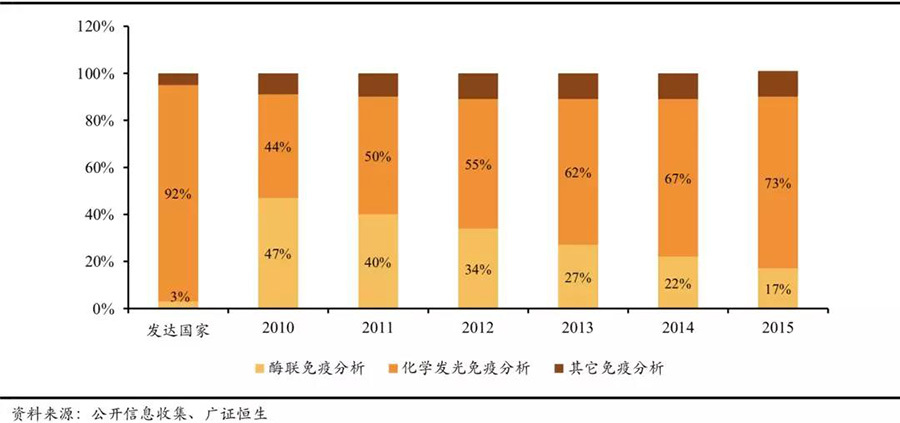

The product technology update and iteration speed in the IVD field is relatively fast.

Currently, chemiluminescent immunoassay technology is rapidly replacing the original enzyme-linked immunoassay technology. Just in the field of immunodiagnostics, it has gone through several technologies: Radioimmunoassay (RIA), immunochromatography, enzyme-linked immunoassay (ELISA), time-resolved fluorescence immunoassay (TRFIA), and chemiluminescent immunoassay (CLIA). Each technological update brings corresponding improvements in detection sensitivity and accuracy, while the development of new technologies can rapidly disrupt and replace past technologies and products.

The technology in the field of immunodiagnostics is rapidly updated and replaced.

China's chemiluminescent immunoassay technology is rapidly replacing enzyme-linked immunoassay technology.

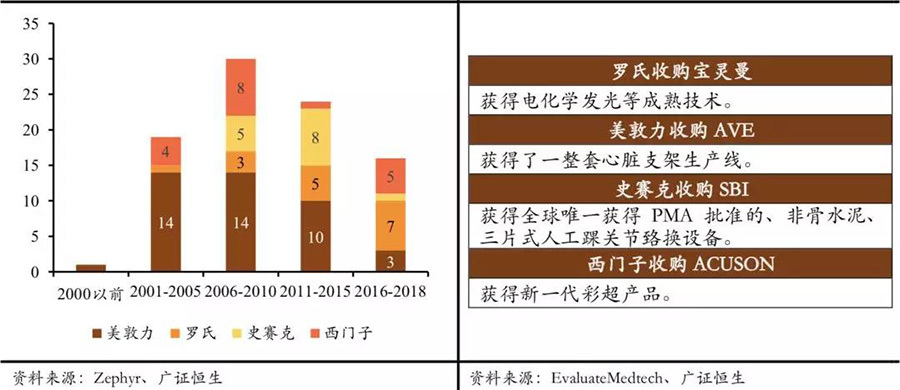

Continuously conducting technological mergers and acquisitions to reduce internal R&D risks. The main methods for major medical device companies to cope with the market share decline caused by technological replacement are twofold: one is to continuously acquire innovative technology companies to reduce internal R&D risks and maintain relative technological leadership. In the past 20 years, medical device industry giants have almost made acquisitions of innovative technology companies every year.

Medical device giants have acquired a large number of innovative technology companies; through acquisitions, medical device giants quickly complete technological updates.

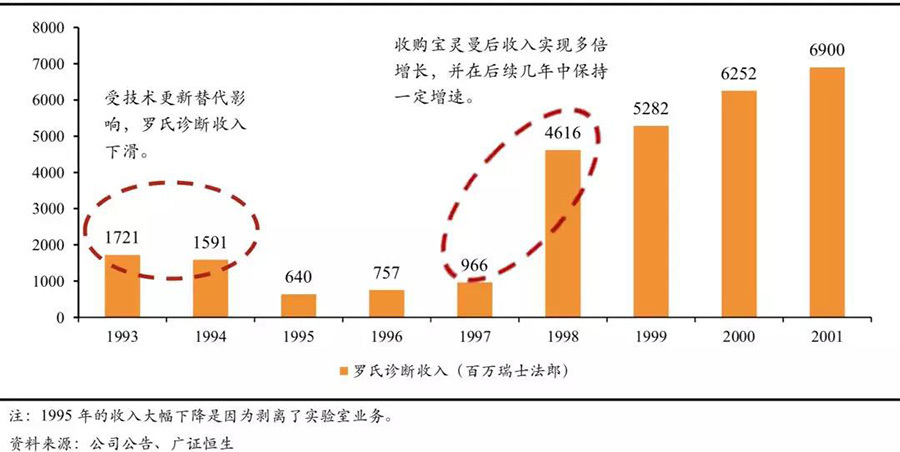

Acquiring competitors to quickly obtain technology and product lines. Among the cases of rapidly achieving technological updates through acquisitions, Roche's acquisition of Boehringer Mannheim is the most classic. In the 1990s, with the maturity of foreign chemiluminescent technology, the competitive landscape of the IVD industry began to reshape rapidly. Competitors like Abbott launched the Axsym series products as early as 1993, followed by the launch of their high-end product Architecti2000 in 1998, which adopted advanced third-generation luminescence technology for direct chemiluminescence. Roche's diagnostic business faced a huge impact, and revenue experienced negative growth. Subsequently, the split of the laboratory business allowed for recovery, and through the acquisition of Boehringer Mannheim, Roche achieved multiple growth and maintained continuous growth in the following decade. Currently, Roche Diagnostics still focuses on electrochemiluminescence as its core product, developed by Boehringer Mannheim in 1996, known as the fourth-generation chemiluminescence technology.

The development history of Roche Diagnostics.

Motive for Mergers and Acquisitions Two: The Ceiling Effect in Subfields.

The market size and space in a single field are relatively limited. Although the global medical device market has reached $400 billion, there are many types of medical device products with significant differences between them. These include relatively simple products like hemostatic sponges and disposable syringes, as well as complex large devices like medical magnetic resonance imaging equipment (MRI). The five largest market segments—IVD, cardiovascular, medical imaging, spinal orthopedics, and ophthalmology—account for about 50% of the market share. At the same time, the growth rate of the medical device market remains around 4%, and the medical device market, especially in developed markets, is basically in a mature stage. As the 'giants' grow larger, their demand for space becomes even more intense.

The medical device industry is basically in a mature stage, and there are many subfields in the medical device industry.

Mergers and acquisitions are essential for development; they are not only for expansion but also for survival. Additionally, in terms of competitive landscape, after decades of development, the global medical device market has become highly concentrated, especially in the main subfields of IVD, cardiovascular, spinal orthopedics, and medical imaging, where the CR10 exceeds 75%. The major companies have basically reached the ceiling of their achievements. At the same time, due to the rapid maturity of technology, short product iteration cycles, severe functional homogenization, and market pricing characteristics, medical device companies are easily threatened by external competition, and market competition can easily deteriorate. Therefore, the development of medical device companies is like rowing upstream; if they cannot further expand their market share, fierce external competition will quickly lead to a decline in market share.

The subfields are in an oligopolistic market (in millions of dollars, the market share of industry giants is challenged and has declined).

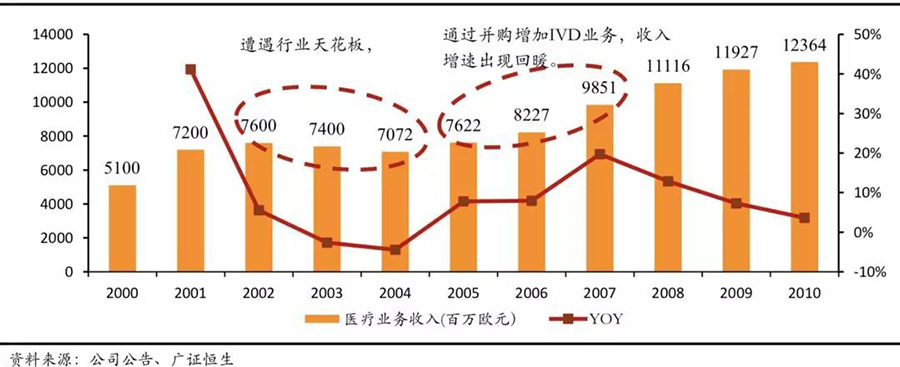

Cross-industry and cross-track mergers and acquisitions are the main ways for industry giants to break through their industry ceilings. In addressing the ceiling issue in subfields, the most common approach among medical device giants is cross-track or even cross-industry mergers and acquisitions. In the past 20 years, the four major medical device giants have engaged in varying degrees of cross-industry mergers and acquisitions, with Siemens' expansion in the IVD field being the most typical. Siemens' medical imaging business began in 1877, and it launched the first X-ray inspection device in 1896, maintaining a leading position in the medical imaging field. However, after 2002, due to the constraints of the industry ceiling and intensified competition from General Electric and Philips, Siemens' market share declined, and revenue showed negative growth. Subsequently, Siemens began to strengthen cross-industry mergers and acquisitions, acquiring Diagnostic Products Corporation, Bayer Diagnostics, and Dade Behring between 2005 and 2006 to enhance its IVD business. Thanks to the successful completion of these acquisitions, Siemens Medical's revenue returned to growth and has maintained high growth in the following years.

Siemens Medical Business Revenue Development

Addressing the issue of revenue hitting a market ceiling by expanding into emerging markets. To hedge against the industry ceiling issue in developed countries, medical device giants tend to explore emerging markets such as developing countries, in addition to cross-border mergers and acquisitions. This is also the reason for the significant increase in the number of merger and acquisition targets in the Chinese market in recent years.

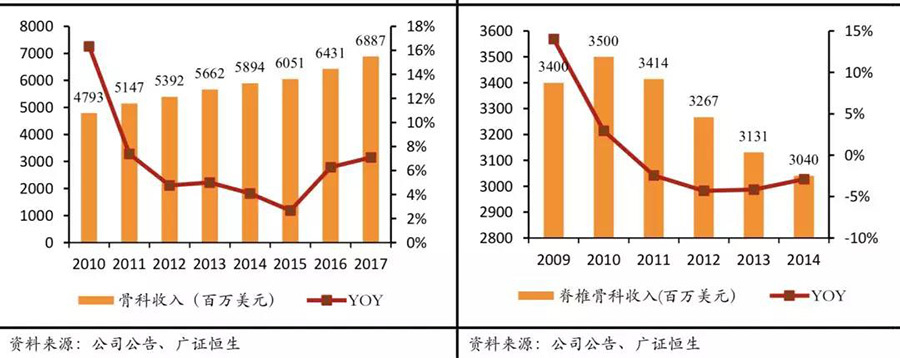

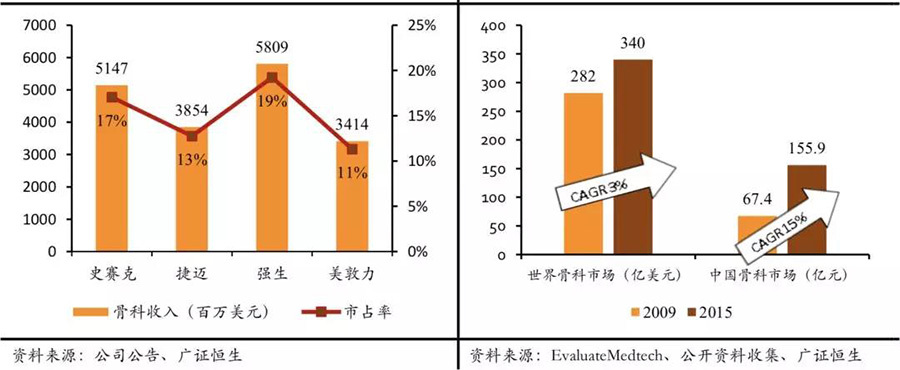

Giants like Stryker and Medtronic have strengthened their mergers and acquisitions in the Chinese market. Among them, mergers and acquisitions in the orthopedic field are quite typical. In 2011, orthopedic industry giants such as Stryker and Johnson & Johnson basically reached their industry ceiling, with the four major orthopedic giants holding a global market share of over 10%. At the same time, the global orthopedic market is basically maturing (6-year CAGR of 3%), and only emerging markets can maintain double-digit high growth, with China's 6-year CAGR at 15%. Therefore, in the following years, due to the constraints of the industry ceiling, the orthopedic revenues of giants like Stryker and Medtronic have shown a certain degree of slowdown or even decline. To hedge against the decline in orthopedic business caused by the industry ceiling, Medtronic and Stryker acquired Chinese orthopedic device companies Kanghui Holdings and Chuangsheng Medical, respectively. We believe that the initiators of these two mergers and acquisitions are optimistic about the high growth in emerging markets like China and aim to hedge against the impact of slowed business growth after reaching the industry ceiling.

Orthopedic giants have basically reached the industry ceiling & emerging markets represented by China are developing rapidly

Stryker's orthopedic revenue growth has slowed & Medtronic's orthopedic revenue decline has narrowed after multiple acquisitions

Source: Guangzheng Hengsheng